Overview Overview

Supporting rapid response to retrospective prior-year corrections

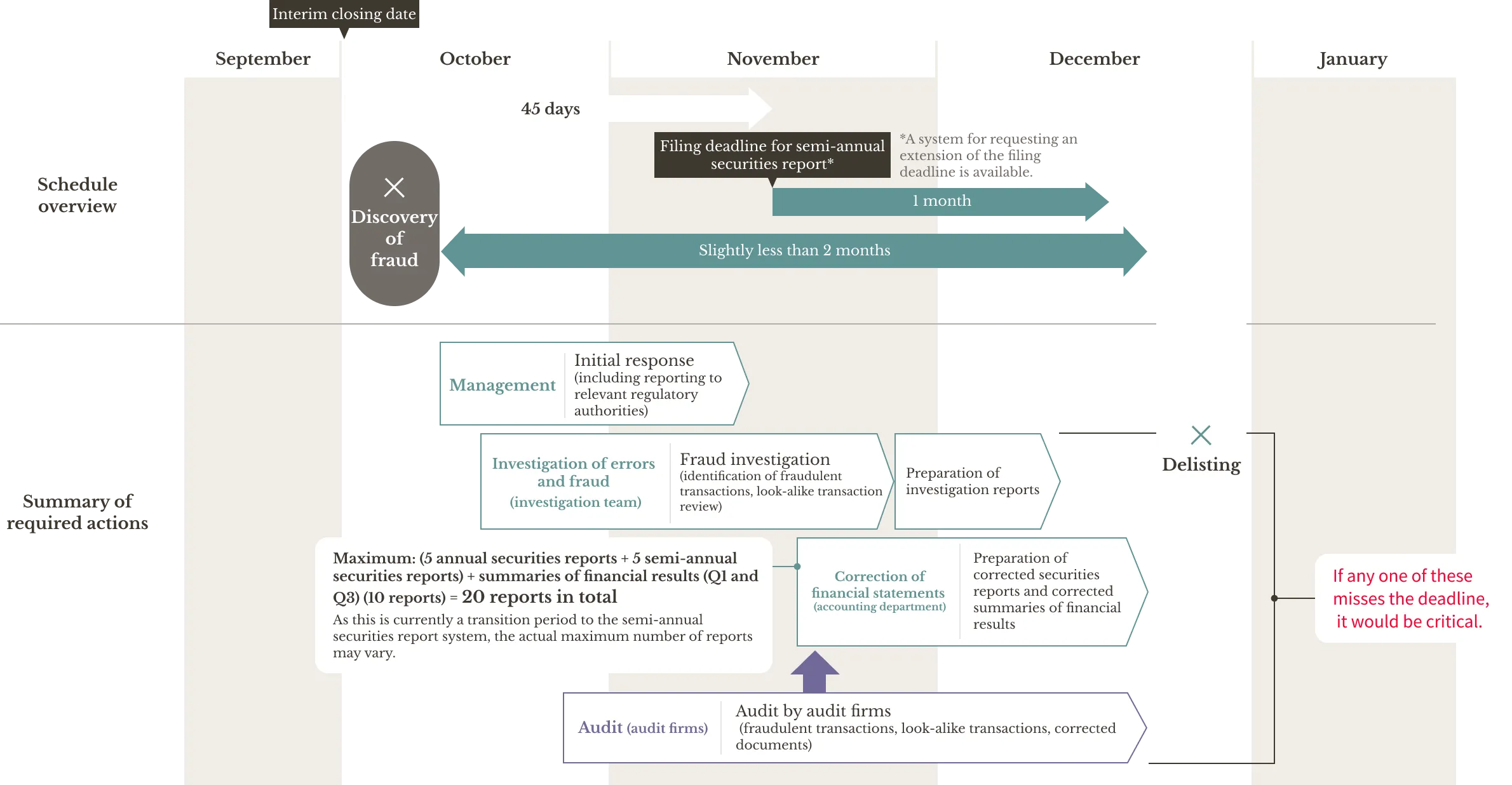

Since the publication of the Accounting Standard for Accounting Policy Disclosures, Accounting Changes and Error Corrections (Accounting Standards Board of Japan [ASBJ] Statement No.24) and its Implementation Guidance (ASBJ Guidance No. 24), when there are changes in accounting policies or presentation methods, or corrections of prior‑period errors, entities are required to revise accounting treatments or presentation as if the new accounting policies or presentation methods had been applied retrospectively to past financial statements (hereinafter, “retrospective prior-year corrections”). In particular, when errors or fraud from past periods are discovered and retrospective corrections of prior‑year financial statements becomes necessary, the greatest challenge in the entire process is time. To maintain listed status, it is an essential condition to execute high‑volume tasks—such as investigation response, corrections of financial statements, and audit response—effectively within a short timeframe and to submit all required disclosure documents (including amended securities reports) by the deadline.

Moreover, in retrospective prior-year corrections, it is common for multiple parties (including accounting personnel, corporate managers, audit firms, regulatory authorities, and investigative committees) to conduct their respective deliberations simultaneously. Timely and appropriate information sharing with all relevant stakeholders, as well as swift and coordinated collaboration, is indispensable. We have accumulated extensive experience since the initial application of these standards, enabling us to provide effective and efficient support for any case involving retrospective prior-year corrections.

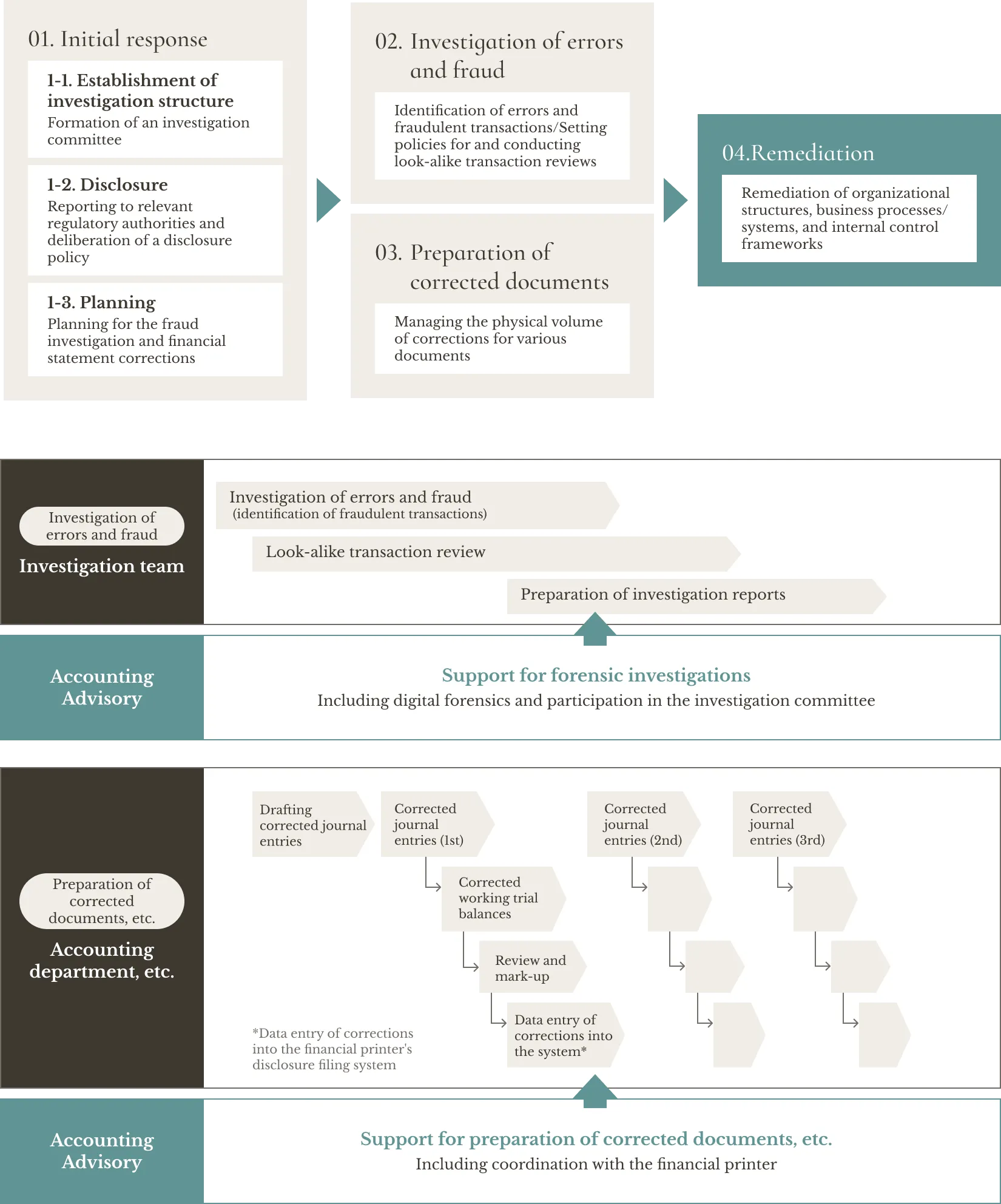

Main process

Schedule example

Case where an error (or fraud) in prior-year financial results is discovered during the interim closing

Key Features Feature

0 1

Rapid response for retrospective prior-year corrections

Retrospective prior-year corrections require high-volume tasks, including investigation response, corrections of financial statements, and audit response—to be carried out efficiently within a tight timeframe. Our experienced team of specialists prepares necessary documents, such as corrected reports, within the deadline and achieves the rapid response essential for maintaining listing status.

0 2

Support for coordination with numerous stakeholders

Retrospective prior-year corrections involve multiple parties—including accounting staff, corporate managers, audit firms, regulatory authorities, and the investigation committee. In such engagements, the speed of information sharing and decision-making is critical. We support timely and appropriate coordination with all relevant parties to keep the process on a smooth track.

0 3

Precise support based on extensive practical experience

Drawing on our experience in numerous projects since the adoption of the applicable standards, we provide effective and efficient support even for complex error corrections and responses to fraud.

Scope of Services Our Service

-

0 1

Support for initial response

-

0 2

Overall coordination and implementation support for retrospective prior-year corrections

-

0 3

Support for conducting fraud investigation

-

0 4

Support for implementing digital forensics

-

0 5

Support for preparation of corrected working trial balances and corrected reports

-

0 6

Support for business process improvement and internal control enhancement, etc.

Service

- IFRS / U.S. GAAP / New Accounting Standards

- Financial Closing Support (Japan / Overseas)

- IPO (Japan / Overseas)

- Fraud Response and Prior Period Restatements

-

- Prior period restatement support

- Fraud investigation and response support

- Fraud and error recurrence prevention support

- Management Accounting

- Financial Advisory